Expenses will being capped in 2015 in VietNam

From 2014 to now, with following related circulars regulating about this issue: 78/2014/TT-BTC, 119/2014/TT-BTC, 151/2014/TT-BTC, 26/2015/TT-BTC and recently 96/2015/TT-BTC, Expenses that being capped for the financial year have changed something. So, We would like to summarize th detail of capped expense as below:

Leagal basis for Expenses will being capped in 2015 in Vietanm

– Capped at 15% with these expenses: Advertising, marketing, promotion, commission; reception, grand opening, conference expense; marketing support expense, Cost support expense; Gifts and presents to customers.

| But from 1/1/2015 with those above expenses: Advertising, marketing, promotion, commission; reception, grand opening, conference expense; marketing support expense, Cost support expense; Gifts and presents to customers which relating to the business operation of the company will not be capped at 15%. (According to Law number 71/2014/QH1 – Amendment to Tax Law). |

Advertising, marketing, promotion, commission being capped include:

– Insurance commissions according to Insurance business law, commissions paid to agents that selling goods and services at setting price

– Commissions paid to multilevel selling distributors. For business which receives commission has to declare this amount to taxable income, for individual who receives commission has to deduct PIT liability before payment. – Expenses occur inside or outside Vietnam (if any): + Market research expense: polls, surveys, interviews, collect, analyse and evaluate information

+ Development costs, market research supporting expenses + Research, development and market research supporting expenses paid to third consultancy firm; + Display cost, product introduction and trade fair & trade show organizing cost; showroom opening cost, product displaying space renting cost, cost of materials and tools supporting for displaying, displaying products shipping cost….

Note: Payment discount for customers (Not being capped)

Moreover, some other costs that cannot classify as deductible expenses as below:

a.Depreciation equivalent to amount of original cost over 1,6 billion VND/Car applied to car that is from under 9 seats (except: car that is using for transportation, tourism business, hotel, sample car and driving test in car business) – Car from under 9 seats that is specializing in transportation, tourism and hotel services is car which is register under company’s name, in which company business license has one of these business line: transportation, tourism and hotel business. – Transferring or liquidating car with from under 9 seats, the residual value is determined equal to (=) original cost (-) accumulated depreciation until the time of transferring or liquidating.

Example: Buying a car under 9 seats with original cost of 6 billion VND, depreciation with 1 year then liquidating that car. Accumulated depreciation is 1 billion VND (equivalent to 6 year time period of depreciation). Depreciation that beyond the tax policy is 1,6 billion VND/6 years = 267 million VND. Liquidate amount is 5 billion VND. Income from liquidating of the car = 5 billion – (6 billion – 1 billion) = 0

b.Uniform expense for Staffs: – Expense spends for Uniform in kind for Staffs without invoice and documents attached. – Expense spends for Uniform in cash for Staffs > 05(five) million VND/person/year. – If Expense spends for Uniform both in cash and in kind for Staffs then maximum amount for recognizing as deductible expense is not over 05(five) million VND/person/year.

| Note: According to 2.7 article 4 Circular 96/2015/TT-BTC effective from 6/8/2015. Uniform regulation: – If spending in kind: recognising all as deductible expense. (If having invoice and documents) – If spending in cash: recognising all amount that is not over 5 million VND/person/ year. – If spending in both cash and kind: recognising maximum amount in cash that is not over 5 million VND/person/ year, and no limitation in amount when spending in kind if with enough invoice and documents. |

c.An amount of expense that is over 01 million VND/month/person for: Voluntary pension contribution, welfare funds, life insurance for employees.

| Note: According to 2.6 Article 4 Circular 96/2015/TT-BTC effective from 6/8/2015.– Remove the cap of 1 million VND/month/person for life insurance buying for employees. All amount will be recognized as deductible expense if the conditions is regulated in these below documents: Labour contract, Collective Labour Agreement, Finance rules, Bonus schemes. |

– Company will build by itself about Bill of raw materials, materials, fuel, energy, merchandises for the purpose of manufacturing and trading. Those norms were built from the beginning of the year or the beginning of the production period and those Bill are being kept at the Company (Some other case will follow the rules regulated by Government)

| Note: According to 2.3 Article 4 Circular 96/2015/TT-BTC effective from 6/8/2015. – Removing the regulation about company’s self-building in Bill of raw materials, materials, fuel, energy, merchandises for the purpose of capping deductible expense for the consumption that over the Bill. – For the spending that is over the norms that being set by Government then these spending in raw materials, materials, fuel, energy, and merchandises will not be classified as deductible expenses. |

e.Traveling expense:

– Traveling and hotel expenses for Staff when on business if with enough invoice and documents will be considered as deductible expenses.

– Procedures for air ticket buying through electronic website: + Electronic air ticket, + Boarding pass + Non-cash payment evidence.

– If cannot collect boarding card from staff, we can use another document such as Business traveling decision instead of.

f.Salaries, wages, bonuses as non-deductible expense:– Salaries, wages and bonuses which is not regulated detail about conditions and amount in Labour contract …

– If in labour contract has a term regarding apartment renting beared by company, then this amount will be considered as salary, wages and not inconsistence with the provisions of Law then this amount will be classified as deductible expense in case it has enough invoice and documents.

– Salary and wage in case of sole proprietorship owner, limited liability with one member (one owner); remuneration paid to founders, council members, board members who does not directly involved in day to day running business.

g.Administrative penalties: – Traffic law violations, – Business registration regulation violations, – Accounting regulation violations, – Tax regulation violations include: Late payment in Tax liabilities and other tax administrative penalties.

h.Input VAT that being deducted or returned. – Input VAT for from under 9 seats car (fixed asset) with amount that excess the regulation.

Bài viết liên quan

How many times for signing seasonal contract with employee

Manufacturing enterprise has seasonal production period can hire workers under seasonal labour ...

Salary expense without insurance contribution as deductible expense?

Enterprise sign Labour contract under the term from over 3 months must contribute insurance for ...

Recognising educational and training cost as deductible expense

In a previous article, we have mentioned the procedures for some deductible expenses in CIT ...

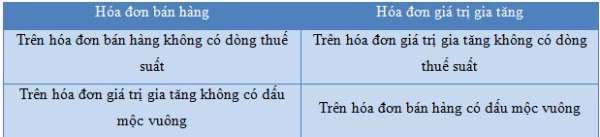

Sự khác nhau hóa đơn bán hàng và hóa đơn giá trị gia tăng

Hóa đơn bán hàng và hóa đơn giá trị gia tăng khác nhau như thế nào? Cách phân biệt Sự khác nhau hóa ...

Các trường hợp và thủ tục xóa nợ tiền thuế, xóa nợ tiền phạt nộp chậm

Khi cá nhân, doanh nghiệp nợ tiền thuế, tiền phạt chậm nộp, tiền chậm nộp tiền thuế, tiền chậm nộp ...

Miễn thuế, giảm thuế theo Hiệp định đối với hãng vận tải nước ngoài

Đại lý thuế Công Minh xin chia sẻ trình từ, thủ tục thực hiện Miễn thuế, giảm thuế theo Hiệp định ...